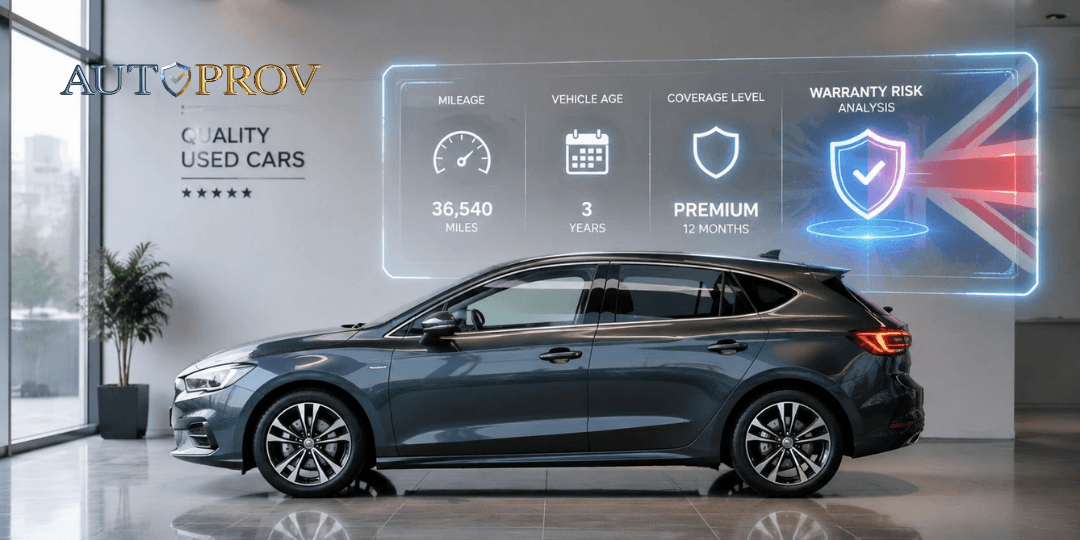

Typical UK used car warranty cost sits around £600 to £750 a year for powertrain cover and £1,000 a year or more for broader cover, while extended cover often lands at £75 to £150 per month and can go above £300 per month for higher-mileage vehicles. For a dealer, though, the key question isn't the sticker price of the warranty. It's the vehicle risk underneath it, because that's what decides whether the cover protects margin or erodes it.

Most popular advice on used car warranty cost still treats warranty like a menu option. Pick a plan, add a monthly figure, move on. That's a consumer framing, and it's weak for trade decision-making.

In a dealership, warranty cost is closer to a live risk signal than a fixed expense. If cover is expensive, it usually isn't because the provider feels generous that day. It's because the car's age, mileage, condition, history quality, or likely repair path makes future claims more probable or more expensive. That distinction matters on every appraisal, every trade buy, and every retail deal.

Why Warranty Cost Is a Risk Metric Not a Price Tag

A lot of dealers still ask the wrong first question. They ask, “What's the warranty going to cost me on this unit?” The better question is, “What is this vehicle telling me about future claims exposure?”

That shift sounds subtle, but it changes how you buy stock. Warranty providers price cover as a risk product, not a goodwill gesture. Higher-risk vehicles are charged more, especially where mileage is higher or service history is weaker, and those same variables already sit at the centre of used-car valuation and future repair exposure according to used car warranty statistics and risk factors.

Why similar cars produce different warranty outcomes

Two cars can look comparable on forecourt pricing and still behave very differently in warranty terms.

One may have:

- Clean mileage progression that makes wear patterns easier to trust

- Consistent servicing that reduces uncertainty around neglected maintenance

- Better component condition visible through preparation and inspection

- Stronger provenance that gives fewer unanswered questions

The other may have:

- High mileage for age

- Patchy paperwork

- Repeated signs of deferred maintenance

- Ownership history that raises questions about why the car moved on quickly

Both cars may retail at a similar headline figure. Only one is likely to protect gross profit after sale.

Practical rule: If warranty pricing jumps sharply on a vehicle, treat that as a signal to re-check the stock appraisal, not just the F&I line.

Margin impact starts before the car is advertised

Many dealers often lose money. They separate acquisition risk from aftersales risk, then wonder why the car underperforms. In practice, they're the same problem viewed from different timings.

If a unit needs expensive cover to make it retailable, that cost belongs in the buying decision. It should sit alongside preparation, tyre position, cosmetic spend, and carrying cost. It isn't an afterthought. It's part of what the car really costs your business.

That matters even more in a market where stock looks expensive at first glance. The average UK car price context is useful, but headline retail value never tells you the full exposure. Dealers don't go wrong only by overpaying for stock. They also go wrong by underestimating what it takes to stand behind it.

Age, mileage and condition are doing two jobs at once

Trade buyers already use age, mileage and condition to value a vehicle. Those same variables also forecast what happens after handover.

That's why used car warranty cost should be read as a compressed risk assessment. It reflects the provider's view of likely claim frequency, likely repair severity, and the confidence they have in the vehicle's background. A low premium doesn't automatically mean a good car, and a high premium doesn't automatically mean a bad one. But either way, the number is telling you something useful.

A warranty price is often the market's blunt answer to a more precise question. How likely is this car to consume profit later?

Deconstructing the Used Car Warranty Cost

When you strip the sales language away, used car warranty cost comes from three moving parts. The vehicle itself. The shape of the cover. The commercial terms behind the provider.

Vehicle factors that move the price first

The first layer is straightforward. Older cars usually cost more to cover than newer ones. Higher-mileage cars usually cost more than lower-mileage cars. Cars with uncertain maintenance histories usually attract stricter underwriting than cars with clean supporting records.

That isn't just because the vehicle is older in a calendar sense. It's because wear accumulates unevenly. A car that has covered hard motorway mileage with proper servicing may present differently from one with stop-start urban use, inconsistent maintenance, and signs of repeated short-term ownership. On paper, both may fit the same broad age band. In risk terms, they don't.

A proper vehicle history check UK process helps here, but basic checks often stop too early. Dealers need more than finance, theft, and write-off markers. They need context around vehicle provenance, mileage pattern, ownership behaviour, and data anomalies that increase claim uncertainty.

Cover level changes the economics

The second layer is the contract itself. Industry benchmarks show powertrain-only cover at around £600 to £750 per year, while broader bumper-to-bumper style cover is often £1,000 per year or more, largely because a wider component set increases expected repair liability after the typical manufacturer warranty period of 3 years or 36,000 miles, as outlined in extended warranty cost benchmarks.

That means the wrong comparison is common. Dealers sometimes compare two monthly prices and assume they're close enough. They aren't, if one product is narrow, heavily excluded, or capped in ways that shift liability back to the customer.

A practical review should always look at:

- Included systems. Engine and gearbox cover is not the same as broad electrical, emissions, infotainment, and ancillary component cover.

- Claim limits. A policy can sound extensive and still fail on payout structure.

- Term and mileage geometry. Time and mileage caps interact. If one runs out quickly, the practical value collapses.

- Exclusions. Wear-related wording often decides whether a customer feels protected or misled.

- Excess and contribution rules. These shape the actual claim experience, not just the brochure.

For dealers who already package maintenance with retail deals, it helps to separate warranty from a car service plan strategy. One controls sudden repair liability. The other spreads routine upkeep. Mixing them up usually leads to bad pricing conversations.

A cheap policy with narrow component cover can create more complaints than a more expensive policy that pays claims cleanly.

Provider and market variables matter too

The final layer is commercial. Warranty providers build in administration, claims handling cost, underwriting appetite, and their own margin requirements. They also react to wider repair conditions in the market.

That's why a quote should never be judged in isolation. It needs to be read against the unit, the likely repair path, and the kind of retail customer who will own it. A premium hatchback with complicated electronics may produce a very different exposure profile from a simpler volume model, even when the age is similar.

Used car warranty cost is never just about what the provider charges. It's about how accurately the quote reflects the risk you are about to retail.

Representative UK Warranty Price Ranges

Most dealers don't need another article that says “it depends” and stops there. You still need usable working ranges.

Independent guidance suggests extended cover typically costs £75 to £150 per month, with higher-mileage or premium vehicles pushing above £300 per month. In annual terms, £900 to £1,800 is a common trade consideration, and whether that's sensible depends on the vehicle's individual repair exposure, as noted in UK extended warranty price guidance.

Representative annual UK used car warranty costs 2026

Vehicle Type Age 3-5 Years (Powertrain Cover) Age 3-5 Years (Comprehensive Cover) Age 6-9 Years (Comprehensive Cover) Small hatchback £600-£750 £1,000+ £900-£1,800 Family saloon or estate £600-£750 £1,000+ £900-£1,800 SUV or premium model £600-£750 £1,000+ £900-£1,800 and can rise above typical monthly ranges on higher-mileage stock These are representative, not underwriting promises. The table is useful as a trading range, but it shouldn't replace unit-level assessment.

Where dealers get caught out

The trap is assuming the range tells you enough. It doesn't. A car near a major maintenance interval, with unclear servicing and uneven mileage progression, may look acceptable in the table and still be poor warranty business.

That's where claim probability matters more than the premium band. If you're already seeing warning signs in prep or provenance, the warranty price is only confirming what the vehicle has been telling you.

One practical cross-check is to compare likely protection cost with common retail repair sensitivities. For example, understanding brake replacement cost in the UK market helps frame customer expectations around routine wear versus genuine warranty events. The distinction matters because many disputes start when buyers assume every post-sale expense should sit inside the warranty.

Representative pricing is a planning tool. It is not a shortcut around appraisal discipline.

The Hidden Economics of Warranty Claims

The headline premium gets too much attention. Claims settlement is where the product either supports the deal or creates friction.

That matters more now because the UK repair market has become more expensive. The Office for National Statistics reported maintenance and repair of personal transport equipment rose by about 7.0% year on year in April 2025, while average labour rates reached £92.05 per hour at independent garages and £196.87 per hour at main dealers, according to UK warranty economics and labour rate context.

Labour rate caps are where cheap cover gets expensive

A low-cost warranty can still be poor value if the labour allowance is unrealistic for the workshop network your customer will use.

Consider the operational problem:

- The customer sees “covered” and expects the repair to be handled in full.

- The repairer bills at real market rates based on current labour conditions.

- The warranty pays to a capped rate that may sit below the actual invoice.

- The shortfall lands somewhere awkward, usually with the customer first and then with your sales or service team dealing with the fallout.

The policy may be technically valid and still fail commercially. That's the point many dealers miss.

Claims experience affects reputation as much as margin

A warranty doesn't just protect against repair spend. It also shapes post-sale sentiment. If claims are slow, heavily challenged, or only partially paid, the customer rarely blames the underwriter first. They blame the dealer who sold the car.

That's why claims guidance should sit inside your retail process. Teams need to know what the product does, what it doesn't do, and how labour caps, diagnostic approval, contribution terms, and excluded items work in practice. For businesses reviewing handling standards and customer expectations under post-sale obligations, warranty claims and CRA 2015 guidance is a useful operational reference.

The cheapest warranty on the invoice can become the most expensive warranty in the business once complaint handling time and customer goodwill are factored in.

What works in practice

The stronger approach is to assess warranties backward from likely claims.

Ask:

- Where will this vehicle realistically be repaired?

- Will the labour cap match that environment?

- Are common failure points likely to sit inside cover?

- Will the customer understand the exclusions before they need to claim?

When those answers are weak, the premium number is almost irrelevant. You haven't transferred risk cleanly. You've only delayed the argument.

Strategic Warranty Management for Dealers

The dealers who manage warranty well don't treat it as an afterthought in F&I. They build it into stock policy, pricing logic, and retail presentation from the start.

That means choosing where warranty should protect margin, where it should support conversion, and where it shouldn't be forced onto a risky unit to make the deal feel safer than it is.

Match cover to stock profile

A single warranty template across the whole forecourt rarely works.

Better operators usually separate stock into practical groups such as:

- Lower-risk core retail stock where broader cover can support confidence and reduce post-sale friction

- Older or higher-mileage units where narrow but clear protection may be more rational than broad promises

- Premium or technically complex vehicles where claims handling quality matters more than a superficially low premium

The key is consistency. If your buying team, prep team, and sales team all use different assumptions about risk, warranty spend becomes reactive and messy.

Negotiate from evidence, not opinion

Providers respond better when a dealer can show disciplined stock selection. Clean provenance, coherent appraisal notes, stronger service-history standards, and fewer obviously marginal cars all improve the quality of the conversation.

Useful habits include:

- Tracking claim themes by vehicle type and age band

- Reviewing declined claims to identify recurring product mismatch

- Separating wear-and-tear complaints from genuine covered failures

- Feeding claims learning back into buying decisions

This is what makes warranty management strategic rather than administrative. The warranty book becomes feedback on how well the business is buying.

Sell clarity, not reassurance

Retail teams often default to vague comfort language. That's what causes trouble later. Customers don't need broad promises. They need a plain explanation of what the product is for, where the limits sit, and how to claim properly.

That usually means:

- explain the difference between warranty and maintenance

- explain any labour cap or approval process before handover

- explain why one car receives different cover from another

When customers understand the structure, disputes tend to be more manageable. When they only hear “you're covered”, every later exception feels like a breach.

Reducing Exposure with Vehicle Risk Intelligence

The cleanest way to control used car warranty cost is to reduce bad uncertainty before you buy the vehicle.

That's the part too many businesses still skip. They run a basic history check, confirm the obvious markers, and move on. But warranty exposure often sits in the grey areas that basic checks don't explain well enough. Ownership churn. Mileage pattern irregularity. MOT history behaviour. Incomplete provenance. None of those automatically make a car unretailable, but they do change how intelligently you should price and protect it.

The broader market context reinforces that point. The average used car age in the UK was 9 years 7 months, and trade buyers need to judge whether a vehicle's mileage pattern and ownership history make any warranty economically rational, especially when older vehicles keep wear-related risk in circulation, as highlighted in used car market age and risk profile analysis.

Basic checks answer less than dealers think

A standard used car history report may tell you whether the car has finance, theft markers, or insurance history. That's useful, but it doesn't necessarily tell you how the vehicle behaved through time.

Dealers need dealer vehicle checks that answer more practical questions:

- Ownership pattern. Was the car held normally, or moved on quickly and repeatedly?

- Mileage logic. Does the recorded progression make sense for age and use?

- MOT signal quality. Are advisories recurring in a way that suggests deferred maintenance?

- Provenance strength. Does the background reduce uncertainty or increase it?

Those are motor trade risk questions, not just compliance questions.

Better data creates better warranty decisions

A good appraisal process should treat warranty suitability as an output of vehicle intelligence.

That means using:

- Mileage check UK data to test whether odometer position is only plausible or actually coherent

- Vehicle provenance analysis to understand how the unit moved through the market

- Trade vehicle intelligence to identify patterns that don't show up in a simple pass/fail report

For teams building internal research workflows around public records, MOT data, and structured source capture, a tool such as Web Scraping API for RAG can help organise evidence gathering around repeatable decision processes.

If you need a rich warranty to make a weak car feel safe, the problem is usually the car, not the warranty.

A stronger buying model starts before valuation and carries through to retail pricing. If you want a deeper standard for advanced vehicle provenance checks, the key is to move beyond static history results and look for behavioural risk in the record.

That's where warranty cost becomes useful. Not as a selling figure, but as confirmation of what the vehicle's data was already saying.

AutoProv helps UK dealers, motor traders, and buying teams assess vehicle provenance, mileage anomalies, ownership patterns, and wider risk signals before capital is committed. If you want sharper decisions on stock acquisition and fewer surprises hidden behind warranty spend, review how AutoProv supports trade-focused vehicle intelligence at the point of purchase.

Frequently Asked Questions

AI-Generated Content Notice

This article was created with the assistance of artificial intelligence technology. While we strive for accuracy, the information provided should be considered for general informational purposes only and should not be relied upon as professional automotive, legal, or financial advice. We recommend verifying any information with qualified professionals or official sources before making important decisions. AutoProv accepts no liability for any consequences resulting from the use of this information.

From our AI insights

- Understanding Black Box Car Insurance for Young UK Drivers

Discover how black box insurance can benefit young drivers in the UK by reducing premiums and promoting safer driving.

- Navigating Road Risks: Seasonal Insurance Strategies

Explore how UK traders can adjust car insurance to mitigate seasonal risks effectively.

- Essential Car Insurance Tips for UK Traders

Discover unique car insurance insights for UK traders, focusing on regulations and practical advice.

Related Articles

Understanding UK Car Insurance: Types and Legalities

Explore the UK car insurance sector, types of coverage, and the legal implications of incorrect coverage.

How to Check If a Car Is Insured in the UK | Easy Guide

The quickest and most reliable way to check if a car is insured is by using the Motor Insurance Database (MID) online. All it takes is the vehicle's registration number to see if a valid insurance policy is on record. Remember, driving without at least third-party insurance is a serious offence here in the UK.

Hit by an uninsured driver: UK accident rights & claim guide

Being hit by an uninsured driver is a deeply frustrating experience. The shock of the accident is bad enough, but finding out the other party has no insurance just adds a whole new layer of stress and confusion. Suddenly, the straightforward path to getting your car fixed seems to vanish. This guide is here to cut through that noise and show you that you're not out of options.

Published by AutoProv

Your trusted source for vehicle intelligence