Thinking you can get by with your personal car insurance for your motor trade business is a critical, and surprisingly common, mistake. The moment a car is used for business, that personal policy is effectively worthless. Proper business insurance car cover isn’t just a nice-to-have extra; it's a legal and financial must-have, built specifically for the unique risks you face every single day. Without it, your business is dangerously exposed.

Why Your Personal Policy Fails Your Motor Trade

It’s easy to fall into the trap of thinking your personal car insurance provides some sort of safety net. The reality is, the two are worlds apart, each designed to cover completely different scenarios. A personal policy is priced for predictable, low-risk use—the daily commute, school runs, or trips to the supermarket. It was never designed to handle the fast-moving, higher-risk world of the motor trade.

Imagine this: you've just picked up a new vehicle at auction. The second you drive it off the lot, your personal insurance is almost certainly void. It has no provision for covering trade stock, customer test drives, or vehicles sitting on your forecourt. An accident in any of those situations would leave you personally on the hook for every penny, a scenario that could easily cripple your business.

The Clear Line Between Personal and Business Use

Insurers draw a very hard line between personal and commercial use for one simple reason: risk. The day-to-day activities of running a motor trade business introduce a whole new level of risk that personal policies just aren't built—or priced—to cover. This is precisely where a dedicated business insurance car policy steps in.

Think about the things you do every week that would give a personal insurer nightmares:

- Driving a constant rotation of different, unfamiliar vehicles.

- Letting prospective buyers test drive cars from your inventory.

- Moving vehicles between your premises, auctions, and customer addresses.

- Storing high-value stock on a forecourt or in a garage, where it's a target for theft or damage.

A standard personal policy is designed for one person and one car in predictable circumstances. A motor trade business is the exact opposite: multiple vehicles, multiple drivers, and constant public interaction. It’s a completely different risk profile that demands specialised commercial cover.

The Role of Due Diligence in Managing Risk

This is exactly why insurers place such a high value on proactive risk management. When you apply for a business policy, they’re not just looking at your cars; they’re assessing the quality of your entire operation. Being able to show that you perform thorough due diligence on every single vehicle you bring into stock can make a huge difference.

Using a service like AutoProv to run comprehensive vehicle checks is a powerful way to prove you're serious about minimising risk. An AutoProv report verifies a car’s entire history, flagging up deal-breakers like outstanding finance, stolen markers, or a hidden write-off history before you buy. This doesn't just protect you from acquiring a problem vehicle; it demonstrates to insurers that you are a responsible, lower-risk operator. For a deeper look into policy specifics, you can learn more about UK car insurance types and legalities in our related guide. This commitment to diligence is fundamental to securing the right protection for your business.

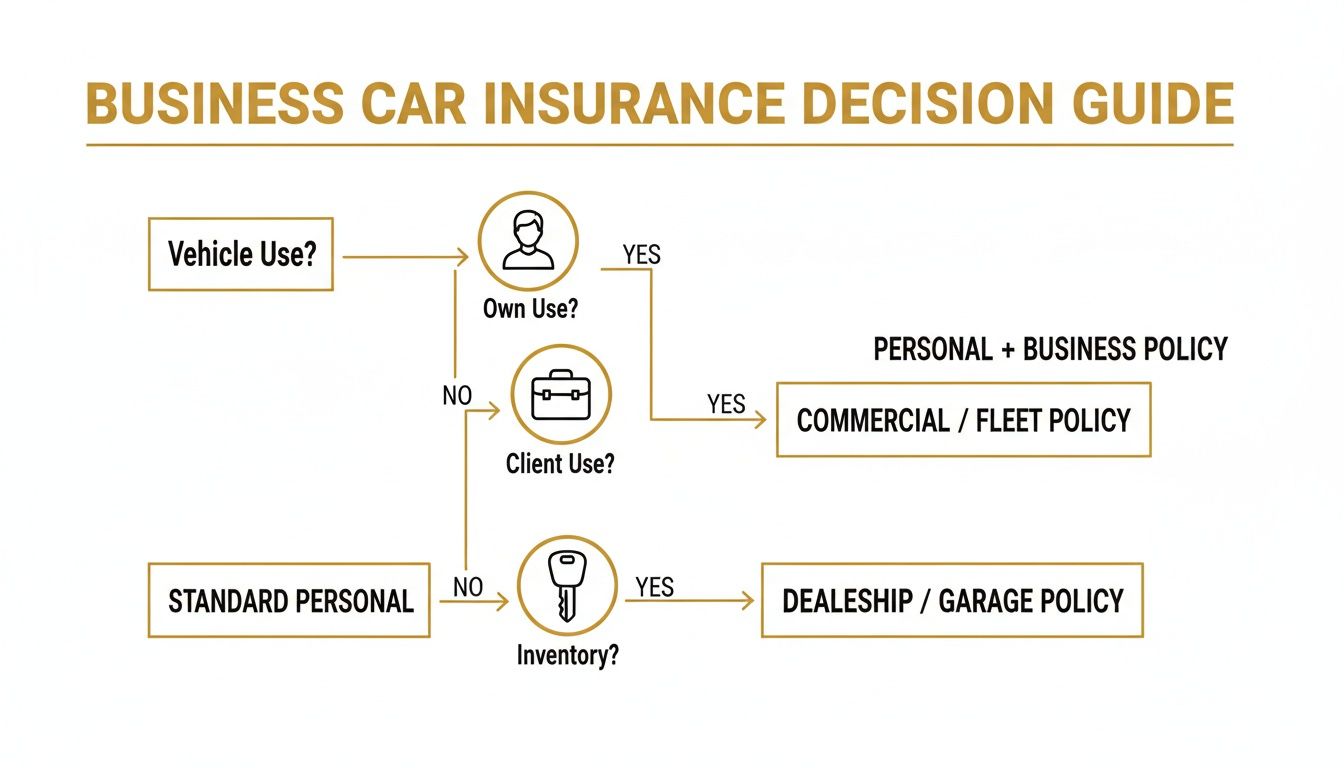

Finding the Right Type of Business Car Insurance

Picking the right business insurance car policy can feel a bit like finding the right key for a very specific lock. Each policy is built for a different job, and using the wrong one leaves your business wide open to risk. It’s all about matching the cover to what you actually do, whether that’s a simple upgrade to your personal policy or a full-blown motor trade package.

Think of standard Business Use cover as a simple add-on to a personal car insurance policy. It's designed for professionals who use their own car for work that goes beyond just commuting to a single office every day. This cover is usually split into three classes, each offering a bit more protection for different types of work.

Understanding Business Use Classes

This is the entry-level stuff, perfect for individuals but completely wrong for motor traders juggling stock. That's a critical distinction.

- Class 1 Business Use is the most basic. It covers you for driving between multiple fixed workplaces or for the odd trip to see a client. An estate agent using their own car for property viewings is a classic example.

- Class 2 Business Use steps it up by letting you add a named driver, like a business partner or colleague, who also uses the car for the same work.

- Class 3 Business Use is for the road warriors—think travelling salespeople who rack up huge mileage as a core part of their role. It acknowledges the much higher risk that comes with being on the road constantly.

While these are great for many professions, they are totally unsuitable for the motor trade. Once you start buying, selling, and managing multiple vehicles, you need something far more robust.

Specialised Motor Trade Policies

The moment you step into the world of holding vehicle stock, your insurance needs change completely. This is where dedicated motor trade policies come in, built specifically for the unique risks of dealership forecourts, service garages, and vehicle fleets.

A Fleet Insurance policy is like a master key for your entire vehicle inventory. Instead of the administrative nightmare of insuring every car individually, a fleet policy covers all vehicles owned by the business under one single, manageable umbrella. That flexibility is absolutely essential when your stock is changing day by day.

For businesses like independent used car dealers or franchised dealerships, fleet insurance is the backbone of their operation. With over 4.3 million company cars on UK roads, fleet vehicles now account for nearly 60% of all new car registrations. These vehicles cover an average of 18,000 miles a year—more than double the mileage of private cars—leading to much higher risks that only a proper fleet policy can cover. You can explore more about the current state of UK fleet insurance in this 2025 analysis.

A Named Driver policy, on the other hand, is much more restrictive. It only provides cover for the specific people listed on the policy. This can be a decent, cost-effective option for a small business with just one or two designated drivers, but it just doesn't have the flexibility needed for a busy dealership where multiple staff members might need to move cars.

Hire and Reward: The Non-Negotiable Cover

Finally, there’s Hire and Reward insurance, which is a completely different beast. This is a legal requirement for any business that carries people or goods in exchange for cash. This isn't for customer test drives; it's for services where the transportation itself is the product.

Think of it as the mandatory cover for:

- Taxi and private hire services

- Courier and delivery companies

- Haulage and logistics firms

- Removal businesses

Trying to operate in these sectors without Hire and Reward insurance is illegal and comes with severe penalties. It reflects the heightened responsibility and risk you take on when you are commercially responsible for getting passengers or property from A to B safely.

Getting these distinctions right is the first step toward building an insurance foundation that won't let you down. For some extra guidance, check out our article on essential car insurance tips for UK traders to help protect your business even further.

Choosing Your Level of Insurance Cover

Once you’ve nailed down the right type of policy for your motor trade business, the next big decision is the level of cover you need. Think of it like a tiered toolkit—each level up gives you a stronger safety net to protect your vehicles, which are the lifeblood of your business. Getting this right is about aligning your business insurance car policy with your appetite for risk and the realities of your day-to-day operations.

Your choice here directly dictates how your business will bounce back after a prang, a fire, or a theft. Skimping on cover might save you a few quid on the premium, but a single bad incident could leave you facing catastrophic costs. It’s all about striking that smart balance between your upfront costs and the potential financial hit if things go wrong.

Let’s break down what each level really means, so you can decide whether your business needs the bare legal minimum, a sensible middle ground, or the gold standard of protection.

This guide helps simplify things. It connects what you do—whether you’re running around in your own vehicles, handling customer cars, or managing a forecourt full of stock—to the level of cover that makes the most sense. The rule of thumb is simple: the more you have at stake, the more robust your insurance needs to be.

Third Party Only: The Legal Minimum

Third Party Only (TPO) is the absolute rock-bottom level of cover you can legally have to drive on UK roads. Its job is to protect everyone else from you and your drivers, not to protect you or your own property.

If one of your vehicles is at fault in an accident, a TPO policy pays for the repairs to the other person’s car and any compensation for their injuries. Crucially, it provides zero cover for damage to your own business vehicle. If your van is written off in a crash you caused, the bill for repairing or replacing it lands squarely in your lap.

Because of this massive financial exposure, TPO is almost never a smart choice for a professional motor trade business where vehicles are your core assets.

Third Party, Fire and Theft: The Next Step Up

As the name suggests, Third Party, Fire and Theft (TPFT) gives you everything a TPO policy does, but with two vital layers of protection for your own vehicles. It pays out if one of your business cars is stolen or gets damaged in a fire.

This is a much more sensible starting point for any business holding vehicle stock. A fire on your premises or a break-in at your forecourt could wipe out a huge chunk of your assets in one fell swoop. TPFT provides a crucial financial backstop against these specific—and often devastating—scenarios.

For any business managing an inventory of vehicles, TPFT cover is widely seen as the absolute minimum. It shields your stock from two of the most common and costly risks beyond road accidents, giving you a much-needed layer of financial security.

Comprehensive: The Gold Standard of Cover

Comprehensive insurance is the highest tier of protection you can get and is the go-to recommendation for most motor trade businesses. It wraps up all the features of TPFT and then adds cover for damage to your own vehicles, no matter who was at fault in an accident.

This means if your driver causes a collision, your comprehensive policy will cover the repairs to both the third-party’s vehicle and your own. It also typically covers other incidents, like damage from vandalism or a storm. This level of protection ensures your operations can get back on track with minimal financial disruption after something goes wrong. To get a better feel for what this involves, take a look at our guide on the meaning of comprehensive car insurance for UK motor trades.

While comprehensive policies naturally come with higher premiums, they offer the greatest security and peace of mind. For a business whose entire livelihood depends on its vehicles, this level of cover isn’t really a luxury—it’s a sound business investment.

What Really Drives Your Insurance Premiums

Ever pulled back the curtain to see how an insurer actually comes up with your business car insurance premium? It’s not a number plucked from thin air. It’s a cold, hard risk assessment where every single detail of your operation is put under the microscope. Grasping this process, known in the trade as underwriting, is the key to influencing the final price you pay.

At its core, underwriting is an insurer’s attempt to predict the future. They’re sizing up your business, from the drivers you’ve got on the books to the cars sitting on the forecourt, to calculate the odds of you making a claim. And in a market this big, the stakes are seriously high.

The UK motor insurance market is a beast, valued at £21.9 billion after a 14.6% rise, and it’s set to climb to £26.2 billion. With claims payouts hitting a record £11.7 billion and the average repair bill now costing £7.7 billion, insurers are more obsessed than ever with pricing risk down to the last penny. You can get more of the story from these UK car insurance statistics and market trends on Uswitch.com. All that financial pressure means every detail you give them can either work in your favour or against you.

Driver and Business Profile Factors

The people behind the wheel are one of the biggest variables an insurer has to wrestle with. A business running a tight ship with a team of experienced drivers over 25, all with clean licences, looks like a much safer bet than one relying on younger, less experienced staff.

Here’s what they’ll zoom in on:

- Driver Age and Experience: It’s a blunt statistical fact—younger drivers have more accidents. That reality translates directly into higher premiums.

- Driving History: Any claims, driving convictions, or penalty points on a driver's licence will wave a massive red flag to an underwriter.

- Business Claims History: Your own track record is paramount. A low claims history is proof you run a professional outfit, whereas frequent claims will send your renewal quotes through the roof.

- Voluntary Excess: Stepping up to a higher voluntary excess—the bit you agree to pay towards any claim—shows the insurer you’re sharing the risk. This simple move can bring your premium down.

These factors all get blended together to create a single risk profile for your entire business. A clean sheet across the board sends a clear signal to the underwriter: this is a responsible operator who deserves a better rate.

An underwriter's job is to balance the premium they charge against the potential cost of a future claim. Every piece of positive data you provide, from driver history to vehicle security, helps tip that balance in your favour.

Vehicle and Location Specifics

Beyond your drivers, the metal itself—and where you keep it—plays a massive part in the calculation. Think about it: a forecourt packed with high-performance sports cars in a high-crime city is a completely different proposition to a stock of family saloons tucked away in a secure rural compound.

Key vehicle-related factors include:

- Vehicle Value and Type: It’s simple maths. More expensive and powerful cars cost more to fix or replace, and they’re a much bigger magnet for thieves.

- Security Features: Insurers love good security. You can earn decent discounts for approved measures like Thatcham-category alarms, immobilisers, and GPS trackers.

- Overnight Storage: Where do the vehicles sleep at night? A locked, secure garage is the gold standard. A well-lit, CCTV-monitored forecourt is the next best thing. Unsecured street parking? That’s the highest risk you can get.

This is where having rock-solid, accurate vehicle data becomes your secret weapon. Proving the quality and low-risk nature of your stock isn’t just about what an insurer sees on the surface; it’s about demonstrating a deeper level of due diligence that stamps out hidden risks before they can turn into expensive claims.

This is why presenting an insurer with an AutoProv report for your vehicles is such a powerful move. By verifying a car's clean history—confirming no mileage discrepancies, no hidden write-off status, and no outstanding finance—you are actively proving that you are a lower-risk client. This kind of documented professionalism can directly influence underwriting decisions, helping you land the more favourable premiums your diligent business practices deserve.

Proactive Strategies to Lower Your Premiums

Treating your business insurance car premium as a fixed, unavoidable cost is one of the quickest ways to hurt your bottom line. A far smarter approach is to see it for what it is: a manageable expense. Taking proactive steps to lower your operational risk makes your business a much safer bet in an insurer's eyes, and that almost always translates into better premiums.

This isn't about cutting corners. It's about showing underwriters that you're a professional outfit that takes risk management seriously. Every decision you make, from driver training to forecourt security, plays a part in the final price you pay. The goal is to prove you’re a partner in preventing claims, not just a customer who might make one.

Smart Driver and Fleet Management

The people behind the wheel are your single biggest risk factor—but they're also your biggest opportunity for saving money. Putting a solid driver management programme in place sends a clear message to insurers that safety is a priority.

Let’s start with the non-negotiables. Regular driver licence checks are a must. They ensure everyone is legally roadworthy and instantly flag up any new penalty points or disqualifications. A formal, written driving policy that lays out the rules on everything from speed limits to mobile phone use is just as important for building a strong safety culture.

Many businesses are also using technology to get an edge. Telematics systems that monitor things like harsh braking, sharp cornering, and acceleration provide a goldmine of data. You can use this intel to pinpoint risky habits and arrange targeted training, which not only makes for safer drivers but also gives you hard evidence to show your insurer come renewal time. Our guide on essential fleet management practices has more on getting this right.

Bolstering Vehicle and Premises Security

How you look after your vehicles when they're parked up is just as crucial as how they’re driven. Good physical security is a straightforward, effective way to reduce the risk of theft and vandalism—two major reasons for insurance claims.

Insurers will often offer real, tangible discounts for approved security upgrades. These are the high-impact ones to consider:

- Vehicle Trackers: GPS trackers massively boost the odds of getting a stolen vehicle back, which cuts the risk of a total loss claim.

- Immobilisers and Alarms: Thatcham-approved systems are a powerful deterrent for opportunistic thieves.

- Premises Security: Simple things like secure, locked storage, decent CCTV, and well-lit premises make your business a much less appealing target.

These aren't just about stopping criminals; they're about proving to your insurer that you've done everything reasonably possible to protect your insured assets.

Your proactive security measures do more than protect your stock; they build a compelling case for your insurer. Each layer of protection, from an immobiliser to a CCTV camera, is a piece of evidence that you are a low-risk, responsible business deserving of a lower premium.

The Power of Proactive Due Diligence

But perhaps the most powerful strategy of all is stopping risk before it even enters your business. Mastering your vehicle acquisition process is the ultimate game-changer. Every car you buy has a hidden history, and if you fail to uncover it, you're essentially importing risk—and your insurer will make you pay for it.

This is where embedding a professional-grade vehicle check into your daily workflow becomes non-negotiable. An AutoProv report gives you instant confirmation of over 40 crucial data points. Before a single penny changes hands, you can know for certain that a vehicle is free of Experian finance markers, has no PNC stolen status, and isn't a previously declared write-off lurking in the system.

This level of meticulous due diligence does more than just stop you from buying a dud. It proves to your insurer that your entire business is built on a foundation of certainty and risk avoidance. By systematically weeding out high-risk vehicles before they ever become your problem, you actively drive down your potential for claims and position your business as a top-tier client. It's exactly this kind of evidence-based risk management that underwriters value most, giving you serious leverage when it's time to negotiate your business insurance car policy.

Securing Your Policy and Staying Compliant

Right, you’ve got a handle on the theory of business insurance car policies. Now it's time to put that knowledge into practice. This is the crucial step where you move from just understanding risk to actively getting it under control. Nailing down the right policy is a process that requires a bit of homework, but getting it right means your motor trade business is built on solid ground.

It all starts with getting your ducks in a row. Before you even think about picking up the phone to a broker, you need a crystal-clear picture of your operation ready to go. This isn't just about making the application process smoother; it's about presenting your business in the best possible light. A well-prepared business always gets better attention and, usually, more accurate quotes.

Gathering Your Essential Information

To get a quote that's actually worth anything, you need to hand over a complete dossier on your business. Insurers will dig into the details because every single data point helps them calculate your specific risk profile. The more thorough you are, the more confidence they'll have in you.

Your information pack should include:

- Complete Driver Details: Get a full list of every potential driver, including their full names, dates of birth, and driving licence numbers. Be ready to share any past claims, convictions, or penalty points for each person.

- Full Vehicle Schedule: Create a clear list of all vehicles you currently hold in stock. For each one, you'll need the make, model, registration number, and its current market value.

- Business Operations Overview: Be prepared to explain exactly what your motor trade activities involve, what your annual turnover looks like, and the physical security you have at your premises.

- Claims History: Have a clear record of any insurance claims your business has made over the last five years.

Having this information organised and ready to go shows you’re a professional and can seriously speed up the whole process.

The most important part of this is absolute honesty. Failing to disclose something important—like a driver's conviction or a previous claim—can make your entire policy worthless. It’s far better to be upfront and pay a slightly higher premium than to have a claim thrown out right when you need it most.

Comparing Quotes and Maintaining Cover

Once your info is ready, it's time to approach specialist motor trade insurance brokers or go directly to insurers to compare quotes. But don't just stare at the price. You need to scrutinise the small print of each quote, paying close attention to the policy excess, any specific exclusions, and the level of cover on offer. A cheaper quote might look tempting, but it could come with a cripplingly high excess or leave a key part of your business completely exposed.

After you've locked in your policy, the job isn't done. Staying compliant is a constant responsibility. The big one here is maintaining continuous cover. Under the UK’s Continuous Insurance Enforcement (CIE) rules, it’s a legal requirement for any vehicle that isn't declared SORN (Statutory Off Road Notification) to be insured at all times. Letting your business insurance car policy lapse, even for a single day, can lead to fines, penalty points, and even your vehicles being seized.

Keeping meticulous records is just as vital. You must tell your insurer immediately about any significant changes to your business. That means adding new drivers, moving premises, or changing the type of work you do. This ongoing chat ensures your cover stays valid and accurately reflects your risk. For a deeper dive into the rules that govern the motor trade, you can explore our article on understanding UK automotive regulations.

Ultimately, the right business insurance is more than just a legal box to tick or another bill to pay. When you combine it with a robust risk management strategy—like embedding AutoProv vehicle checks into your buying process—it becomes a critical investment. This powerful combination protects the resilience, reputation, and long-term success of your entire motor trade operation.

At AutoProv, we provide the certainty you need to buy and sell vehicles with confidence. Our professional-grade reports verify over 40 critical data points in seconds, from Experian finance checks to salvage auction history, helping you avoid costly mistakes and demonstrate best-in-class due diligence. Protect your business and strengthen your insurance profile by visiting https://autoprov.ai.

Frequently Asked Questions

AI-Generated Content Notice

This article was created with the assistance of artificial intelligence technology. While we strive for accuracy, the information provided should be considered for general informational purposes only and should not be relied upon as professional automotive, legal, or financial advice. We recommend verifying any information with qualified professionals or official sources before making important decisions. AutoProv accepts no liability for any consequences resulting from the use of this information.

From our AI insights

- Understanding Black Box Car Insurance for Young UK Drivers

Discover how black box insurance can benefit young drivers in the UK by reducing premiums and promoting safer driving.

- Navigating Road Risks: Seasonal Insurance Strategies

Explore how UK traders can adjust car insurance to mitigate seasonal risks effectively.

- Essential Car Insurance Tips for UK Traders

Discover unique car insurance insights for UK traders, focusing on regulations and practical advice.

Related Articles

Understanding UK Car Insurance: Types and Legalities

Explore the UK car insurance sector, types of coverage, and the legal implications of incorrect coverage.

How to Check If a Car Is Insured in the UK | Easy Guide

The quickest and most reliable way to check if a car is insured is by using the Motor Insurance Database (MID) online. All it takes is the vehicle's registration number to see if a valid insurance policy is on record. Remember, driving without at least third-party insurance is a serious offence here in the UK.

Hit by an uninsured driver: UK accident rights & claim guide

Being hit by an uninsured driver is a deeply frustrating experience. The shock of the accident is bad enough, but finding out the other party has no insurance just adds a whole new layer of stress and confusion. Suddenly, the straightforward path to getting your car fixed seems to vanish. This guide is here to cut through that noise and show you that you're not out of options.

Published by AutoProv

Your trusted source for vehicle intelligence