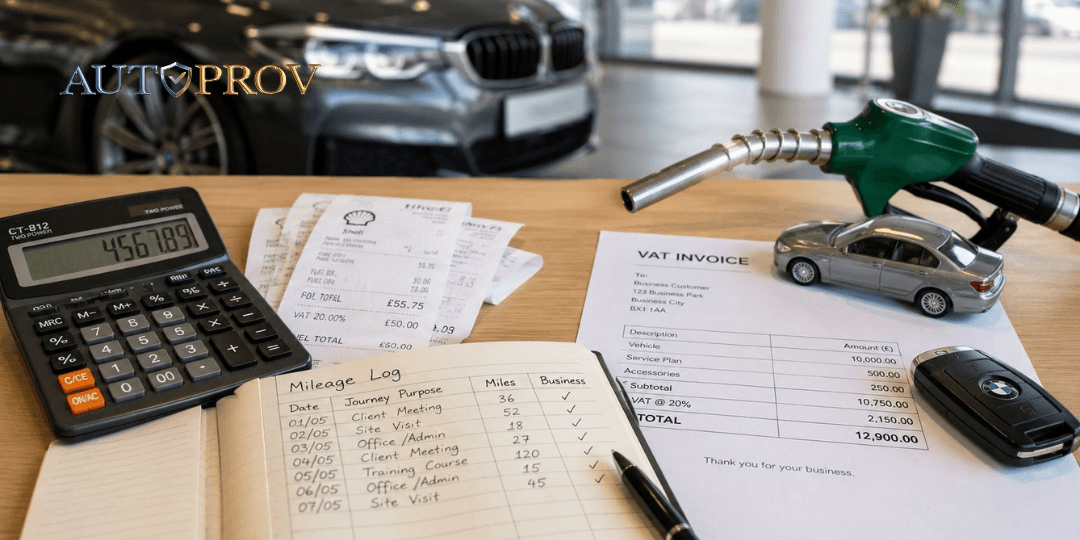

A sales executive takes a demonstrator to a customer appointment, a driver heads to BCA Blackbushe for a collection, and a technician puts road-test miles on a vehicle after repair. All of that mileage costs money. In a VAT-registered dealership, some of that VAT can be recovered. The mistake is assuming the claim is straightforward. It isn't.

In the motor trade, mileage sits right in the overlap between accounts, payroll, fleet control and compliance. If your logs are loose, your fuel receipts are missing, or your team claims against the wrong basis, HMRC won't be interested in what you meant to do. It will look at what you can prove.

Why VAT on Mileage Matters for Your Dealership

Dealerships generate business mileage all day. Sales staff move demonstrators. Buyers inspect stock. Drivers collect and deliver vehicles. Service staff road-test cars after diagnostics or repair. None of that is unusual. What is unusual is finding a dealership that handles the VAT side of mileage consistently across every department.

That matters because claiming VAT on mileage is not the same as reimbursing mileage. Payroll may pay an allowance cleanly enough, but the VAT reclaim sits on a different footing. If your team treats the mileage rate as one simple reclaimable expense, the business drifts into overclaims. If nobody bothers to separate the fuel element properly, you underclaim and leave valid recovery behind.

Where dealers usually go wrong

The trade tends to stumble in a few familiar places:

- Demonstrator use blurs into private use. A sales manager takes a car home, then uses it for customer appointments the next morning. Unless that split is documented, the reclaim position becomes weak.

- Collections are recorded badly. "Auction run" isn't enough. HMRC expects a business purpose that ties back to an actual journey.

- Road tests get ignored. Workshop controllers often think of road tests as operational, not financial. They are both.

- Fuel evidence is scattered. Receipts stay in gloveboxes, card statements sit in accounts, and mileage claims land in payroll with no audit trail.

Dealerships rarely get into trouble because the principle is complicated. They get into trouble because the paperwork doesn't match the reality of how vehicles are used.

There's also a broader fleet cost angle. As more sites run mixed petrol, diesel, hybrid and electric cars, mileage policy starts to affect operating cost decisions, not just expense processing. Anyone reviewing vehicle running costs alongside reimbursement policy should also understand the wider Solana EV total cost of ownership picture, because reimbursement method and vehicle choice increasingly influence each other.

For dealer groups tightening controls, mileage should sit inside the same discipline as vehicle allocation, driver records and operating policy. A practical starting point is treating it as part of wider modern fleet management for UK businesses, not as a standalone expenses chore.

Why finance teams care

A clean process does two things. It protects the reclaim you're entitled to, and it gives you something defensible if HMRC ever asks questions.

In a dealership environment, that matters more than it does on paper. Forecourt use, trade plates, handover runs and workshop test miles create movement that looks ordinary internally but can look vague externally unless it's recorded properly.

Understanding the Core Principle Fuel vs Full Allowance

A sales manager submits 220 miles for auction collections and dealer transfers, payroll pays the standard mileage rate, and someone in accounts tries to reclaim VAT on the full amount. That is the point where dealerships create avoidable exposure.

The rule is straightforward. You cannot claim VAT on the full mileage allowance. HMRC's approved mileage rates cover more than fuel. They also reflect running costs such as wear, insurance, servicing and depreciation. For VAT purposes, only the fuel element is recoverable.

Why HMRC draws that line

From HMRC's perspective, a mileage payment is a mixed amount. One part relates to fuel used on business journeys. The rest is compensation for owning and running the vehicle.

That distinction matters in the motor trade because journeys often look routine internally but involve different VAT treatment in practice. A demonstrator taken to a customer appointment, a collection run on trade plates, and a service adviser using their own car to drop paperwork across town may all be business travel. Even so, VAT recovery still attaches only to the fuel portion.

A practical comparison helps here. Payroll can reimburse the full approved mileage amount under your expenses policy. Finance can only reclaim VAT on the fuel element within that payment, and only where the supporting evidence is in place.

The two accepted approaches

HMRC allows two broad routes for road fuel. A business can reclaim VAT on fuel and deal with private use through a fuel scale charge, or it can reclaim VAT only on the business fuel supported by mileage records and fuel evidence, as set out in HMRC's internal manual on road fuel and input tax.

In dealerships, the second route is often the safer fit.

Vehicle use changes too often for broad assumptions to hold up well under review. Demonstrators move between sales staff. Courtesy cars pick up mixed use. Managers may drive between sites one day and take a vehicle home the next. Hybrid and EV fleets add another layer, because businesses sometimes carry over petrol mileage habits into vehicles where the fuel calculation needs a different approach or no fuel reclaim exists at all.

Practical rule: once a vehicle has any private use, the mileage record becomes evidence, not admin.

What this means on the ground

A buyer driving to inspect part-exchanges, a sales executive doing an out-of-area handover, and a technician carrying out a road test after repair can all generate valid business mileage. The VAT position does not change just because the trip is ordinary in dealership life. The business still has to separate fuel from the wider allowance or reimbursement.

This is also where policy often falls behind operations. Many dealer groups have a mileage process built around employee expenses, but no clear rule for demonstrator use, trade plate movements, or mixed petrol, diesel, plug-in hybrid and electric fleets. If you are reviewing which fuel type works best for a UK dealership fleet, align that decision with your mileage and VAT process at the same time.

If the expense claim says "customer visit" and nothing else, finance has little to defend. If it shows the date, route, purpose, miles, vehicle type, and matching fuel evidence where required, the claim is far easier to support.

Method 1 Using Mileage Allowances and Fuel Rates

A common dealership scenario is a sales executive using their own car to collect a vehicle from auction, a service advisor running paperwork between sites, or a manager taking a demonstrator to a customer event and then switching back into a private vehicle. The mileage payment is straightforward. The VAT claim is not. Under this method, the business reimburses mileage in line with its policy, but only reclaims VAT on the fuel element within that payment.

That distinction matters most in the motor trade because journeys are varied and vehicles are not. One claim may relate to a private petrol car. The next may involve a plug-in hybrid used for a parts run. An EV adds another wrinkle, because there is no fuel element to reclaim through the usual advisory fuel rate approach.

How the method works in practice

The process is simple if finance, payroll and the department approving the trip all use the same rule:

- Record the journey in enough detail to show it was for business. Include the date, start and finish points, purpose, miles, and vehicle used.

- Pay the mileage claim under your dealership policy. Many businesses use HMRC's approved mileage allowance payments as the reimbursement basis.

- Calculate the fuel element only. The VAT reclaim is based on that part of the mileage payment, not the full amount paid to the employee.

- Match the claim to fuel evidence. Keep VAT receipts that support the fuel used across the period.

- Reclaim VAT on the fuel element only.

This usually fits staff using their own vehicles for work, including auction visits, inter-branch meetings, off-site handovers, banking runs, document drops, and occasional collection work where no company vehicle was provided.

What managers often get wrong

The expense is approved correctly, but the VAT entry is wrong because someone treats the whole mileage payment as VAT recoverable. HMRC does not allow that. The approved mileage allowance covers more than fuel. It also reflects running costs such as wear, insurance and depreciation, and those elements do not create a VAT reclaim.

A quick sense-check helps. If a sales manager claims 120 business miles in a private car, the dealership may reimburse the full mileage amount under policy. Finance should then isolate the fuel portion using the correct advisory fuel rate for that vehicle type and engine band, and reclaim VAT only on that amount. That is the figure worth defending in an HMRC review.

Example advisory fuel rates to keep in your finance notes

The rates below are illustrative examples only. Always use the rate in force for the period you are processing.

Example HMRC Advisory Fuel Rates, illustrative examples from Q1 2026 Advisory Fuel Rate Petrol up to 1400cc 14p per mile Petrol 1401cc to 2000cc 17p per mile Petrol over 2000cc 26p per mile For hybrids, use the fuel rate that matches the car's engine and fuel type where HMRC treats it within the advisory fuel rate framework. For full EVs, this method does not produce a fuel VAT reclaim in the same way, because electricity is not treated as road fuel under the normal mileage fuel-rate approach. That catches dealers out when they move part of the management fleet from petrol to electric but keep the old mileage VAT logic.

Where this method works well in a dealership

It suits businesses that want a controlled, repeatable process without collecting every fuel purchase made by staff in their own cars. It is often the cleaner option for sales teams, buyers, group staff moving between sites, and aftersales managers who occasionally use a private vehicle for work.

It is less suitable where vehicle use is blurred. Demonstrators taken home, trade plate movements, and collection drivers swapping vehicles during the day can create confusion over which journeys belong to a private car claim and which belong to a company-fuel process. Draw that line clearly in policy. If a trip is done in a company vehicle, it should not be mixed into an employee's private mileage claim.

I have found that the strongest setups do three things consistently. Department heads approve the business reason for the trip. Accounts check that the fuel evidence exists. Fleet or admin confirm what vehicle was used. That matters even more where the dealership is reviewing benefits and running costs across petrol, hybrid and electric cars. If that review is already underway, align the mileage rules with your UK company car tax policy for dealership vehicles.

Poor records do not always stop the mileage payment. They do weaken the VAT reclaim quickly. If the claim says only "customer visit" and nobody can show the route, vehicle, and supporting fuel evidence, finance has very little to put in front of HMRC.

Method 2 Reclaiming VAT on Actual Fuel Purchases

The alternative is to deal with actual fuel rather than focusing on the mileage allowance route. Under HMRC's business fuel rules, a VAT-registered business can either reclaim VAT on all fuel and then account for private use through a fuel scale charge, or reclaim VAT only on fuel used for business trips. HMRC also requires detailed mileage records and valid VAT invoices for business expense claims, as outlined in HMRC guidance on charging, reclaiming and recording VAT on business expenses.

What this method looks like in a dealership

This approach is usually seen where the business pays for fuel directly. That may be through:

- Fuel cards issued to staff

- Company-paid cards for demonstrators or management cars

- Workshop or driver accounts used for frequent trade movement

- Site-level arrangements for regular collection and delivery runs

The attraction is obvious. If the business already holds the fuel receipts and the vehicles are under tighter control, reclaiming against actual fuel can feel more direct than building the claim through mileage reimbursements.

The trade-off is admin and discipline.

The real comparison

With actual fuel purchases, the records need to stand up on two fronts. First, you need valid VAT evidence for the fuel bought. Second, you still need to show how much of that fuel relates to business use rather than private motoring.

That means the workload often shifts rather than disappears.

Approach What suits it Main pressure point Mileage allowance plus fuel element Staff using personal cars, mixed casual business journeys Correctly isolating the fuel element Actual fuel purchases Company vehicles, regular fuel card use, tighter central control Proving business versus private use and handling the fuel scale charge decision If your demonstrators and manager cars have frequent private use, actual fuel claims can become harder to manage than they first appear.

When this route can make sense

It can suit a dealership with strong central control over vehicle allocation, fuel cards and logs. It can also be practical where company vehicles carry most of the travel burden and where the accounts team already reconciles fuel by vehicle.

But if your operation relies on informal vehicle swaps, unrecorded demonstrator usage or loose trade plate movements, this method exposes those weaknesses quickly. In those environments, the compliance problem isn't the VAT rule. It's the lack of a reliable trail.

That's also why vehicle usage data matters beyond tax. In the motor trade, weak journey records often sit alongside weak stock controls, patchy handover records and blind spots in vehicle provenance. Better internal controls tend to reinforce each other, which is why tax process often ends up touching broader fleet management and tax implications in the UK motor trade.

Essential Record-Keeping for a Watertight HMRC Claim

A sales manager swaps into a demonstrator for a customer visit, a driver heads to auction on trade plates, and a technician takes a hybrid out after a warning light repair. By Friday, everyone knows the vehicles moved for valid business reasons. That is not enough for a VAT file. HMRC looks for a record that shows who travelled, which vehicle was used, why the journey was business-related, and how the fuel element was supported.

What a compliant mileage record should show

In a dealership, the best logs are plain, specific and completed close to the journey date. They should show:

- Date of journey. Record the actual day the vehicle moved.

- Start and finish points. Use real locations, such as "site to Manheim Leeds" or "service department to customer address".

- Business purpose. State the reason clearly, such as customer appointment, vehicle collection, inter-branch transfer, road test after repair, bodyshop estimate, or delivery handover.

- Business miles. Record the mileage for the business journey, not a rough monthly estimate.

- Vehicle details. Registration is the minimum. For trade plate use, add the vehicle identity as well if the plate moved between cars.

- Driver or employee name. HMRC will expect the claim to tie back to a person, not just a vehicle.

The wording matters. "Collect vehicle from BCA Blackbushe" stands up well. "Auction run" does not. "Road test after gearbox diagnosis, fault code check and confirmation" is far better than "test drive".

Motor-trade use needs a bit more discipline than a standard office mileage log. Demonstrators are often shared. Collection drivers move stock between sites. Trade plates can cover several vehicles in a week. If the log only shows miles and a surname, the accounts team is left guessing, and HMRC will not fill the gaps for you.

Keep fuel evidence with the journey record

Fuel receipts and VAT invoices belong in the same file as the mileage support. That applies whether you are reclaiming VAT through the fuel element of a mileage allowance or working from actual fuel purchases for company vehicles.

I would keep the process tight:

- Drivers submit mileage weekly, not at month-end

- Line managers check the business purpose while the trip is still fresh

- Accounts match the claim to the supporting fuel evidence

- Any odd entries are queried before the VAT return is prepared

- Records are filed by employee or vehicle, with trade plate notes where relevant

That last point saves time. A single monthly pile of receipts and handwritten notes is where weak claims start.

Dealership records need to reflect how vehicles are really used

The common gap is not dishonesty. It is informality. A sales executive borrows a manager's demonstrator. A service advisor drops a customer home in a courtesy car. A technician road-tests an EV twice because the first run did not reproduce the fault. All of that can be valid business use, but the record must say so.

EVs and hybrids add another wrinkle. You may have lower petrol or diesel usage across the fleet, but you still need a clear audit trail for vehicles that do use fuel, especially mixed fleets where one manager runs a plug-in hybrid and another still uses a petrol demonstrator. Keep the vehicle type obvious in the log so the accounts team applies the right treatment and does not assume one rule covers the whole fleet.

A good control check is to compare journey logs against stock movement records and a DVLA mileage check process for vehicle history control. The purpose is the same. Build a consistent account of where the vehicle was, when it moved, and why.

Good mileage records also solve operational arguments. If a demonstrator comes back with unexplained miles, or a customer disputes when a collection took place, the answer should already be in your files. That protects the VAT claim and the dealership.

Common Pitfalls and Advanced Motor Trade Scenarios

Most VAT mileage errors in the trade aren't exotic. They're ordinary mistakes repeated for years. The complication comes when those basic mistakes collide with dealer-specific vehicle use.

The pitfalls that trigger problems first

These are the ones I see most often:

- Claiming against the full mileage allowance. This is the classic error. The mileage reimbursement may be right, but the VAT treatment isn't.

- Missing logs for demonstrators. Sales teams often treat demonstrators as semi-permanent cars and stop recording business use properly.

- Loose trade plate records. If the plate movement is recorded but the business journey isn't, the VAT file is incomplete.

- Workshop road tests with no purpose note. A technician may know exactly why the car was driven. HMRC won't unless the log says so.

- Using one rule for petrol and assuming it fits everything else. It doesn't.

Demonstrators, collections and trade plates

A demonstrator is where dealership reality tends to overtake policy. A car may be used for customer appointments, commuting, management oversight and private errands in the same week. That doesn't make VAT recovery impossible, but it does mean the private and business split must be evidenced properly.

Vehicle collections create another weak spot. If one member of staff travels out in a company car and returns in purchased stock, the journey chain needs to make sense on paper. Who drove what, why, and for which business purpose should be obvious from the record.

Trade plates don't change the core rule. They change the operational context. The journey still needs a business purpose, dates, destinations and support for the fuel claim.

The more fluid your vehicle movement is, the less HMRC will accept broad descriptions and assumptions.

Hybrids and electric vehicles need separate thinking

Standard mileage guides frequently prove inadequate for the motor trade. Mixed fleets are becoming normal. Some dealer groups now have petrol sales cars, hybrid management vehicles and fully electric demonstrators all under one policy.

For fully electric cars, one recent UK guide cites HMRC's advisory mileage rate at 4p per mile and notes that this is the total amount claimable for business travel, creating a different outcome from petrol or diesel claims, as discussed in Ultra Accountancy's guide to VAT on business mileage.

That matters because finance teams can't just port petrol logic across to EVs and assume the same claim structure applies. Hybrids also need care because vehicle class and fuel type affect how the claim is handled in practice. If your site runs a mixed forecourt and mixed staff fleet, your mileage policy should identify those differences clearly rather than burying them in one generic form.

What works best

For most dealerships, the strongest setup has three features:

- One mileage policy for staff

- One approval standard for department heads

- One central finance review before VAT is reclaimed

If those three parts don't line up, the business ends up with inconsistent claims and avoidable exposure. The good news is that this is fixable with process, not guesswork.

AutoProv helps UK dealers make better vehicle decisions before risk turns into cost. If your operation is tightening controls around stock acquisition, mileage anomalies, ownership patterns and broader trade vehicle intelligence, AutoProv gives the motor trade a clearer view of vehicle provenance and hidden risk signals that basic checks often miss.

Frequently Asked Questions

AI-Generated Content Notice

This article was created with the assistance of artificial intelligence technology. While we strive for accuracy, the information provided should be considered for general informational purposes only and should not be relied upon as professional automotive, legal, or financial advice. We recommend verifying any information with qualified professionals or official sources before making important decisions. AutoProv accepts no liability for any consequences resulting from the use of this information.

From our AI insights

- Understanding Distance Sale Regulations for UK Car Dealers

Explore UK distance sale rules for car traders and buyers, including benefits, pitfalls, and protection rights.

- Navigating the Consumer Rights Act for Electric Vehicle Sales

Understand how the Consumer Rights Act 2015 impacts electric vehicle transactions for UK dealerships.

- How the Consumer Rights Act 2015 Impacts Used Car Sales

Explore how CRA2015 affects used car sales, protecting buyers with specific rights.

Related Articles

Understanding the Consumer Rights Act 2015 in the UK Motor Trade

Explore the Consumer Rights Act 2015 and its impact on UK car buyers and sellers, offering essential protections and insights.

Understanding UK Automotive Regulations

Explore the complexities of automotive regulations in the UK, covering DVLA, FCA, MOT, and more.

What is a V5C Document: A Quick UK Log Book Guide

If you've ever bought or sold a car in the UK, you've definitely come across the V5C. It's often just called the 'log book', and it’s the official Vehicle Registration Certificate issued by the DVLA.

Published by AutoProv

Your trusted source for vehicle intelligence